Payments have gotten complicated. What used to work one processor, one checkout form, done simply doesn’t cut it anymore. Merchants scaling across borders in 2026 are dealing with tighter regulations, smarter fraud, and customers who abandon carts the second something feels slow or unfamiliar. Getting acquiring card payments right is no longer a back-end concern. It’s a growth lever.

Card Acquiring: The Part of Payments Most Merchants Ignore

Most businesses set up a payment processor and move on. But understanding what’s actually happening under the hood changes how you manage costs, approvals, and risk.

So What Does a Card Payment Acquirer Actually Do?

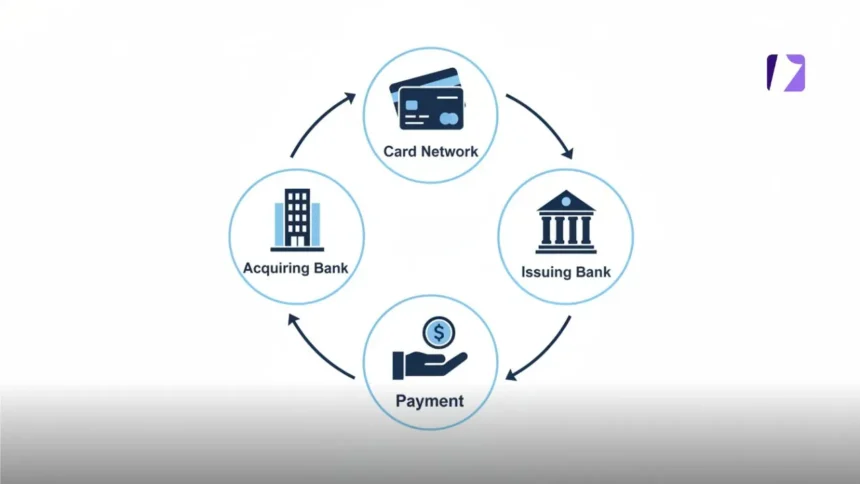

When a customer pays by card, their money doesn’t teleport into your account. It travels through a chain: your acquiring bank, the card network (Visa, Mastercard, etc.), and the customer’s issuing bank. The card payment acquirer sits at the center holding your merchant account, monitoring for compliance, and taking on financial responsibility for the transactions it processes.

A poorly chosen acquirer quietly costs you money in ways that don’t always show up on a single invoice. Lower approval rates, slower settlements, surprise chargeback fees these all trace back to the acquirer relationship.

Why Sticking With One Acquirer Is a Growing Risk

Single-acquirer setups made sense when businesses were smaller and mostly domestic. In 2026, they’re a liability. Here’s what’s at stake:

- Downtime exposure: If your acquirer goes offline, every transaction during that window is gone

- Weaker cross-border approvals: International routing consistently underperforms local acquiring

- No negotiating leverage: One provider means no competitive pressure on fees or terms

- Limited routing flexibility: You can’t send transactions to whoever performs best for that card type

The fix isn’t complicated in theory: connect to multiple acquirers and route smartly. That’s where payment orchestration comes in.

Smarter Ways to Handle Acquiring Card Payments at Scale

Scaling globally means the old “set it and forget it” approach breaks down fast. The merchants pulling ahead are the ones treating acquiring card payments as an active strategy, not a solved problem.

Payment orchestration platforms (POPs) connect multiple acquirers and route each transaction based on real-time data card type, currency, geography, and live performance metrics. No single acquirer wins on every transaction type. One might be great for European debit cards but weaker on US corporate cards. Orchestration captures the best outcome per payment rather than averaging across one provider’s general performance.

Three Things That Actually Move Authorization Rates

Authorization rates are one of the most under-monitored numbers in a payment operation. When a card is declined, the merchant often loses that customer entirely not just that sale. A few things make a real difference:

- Local acquiring: Routing through a domestic acquirer in the customer’s country improves approval odds, because issuing banks trust local transactions more

- Network tokenization: Replacing raw card numbers with Visa or Mastercard tokens has shown meaningful authorization improvements and reduces security exposure

- Better transaction data: Submitting customer email, device ID, and IP address gives issuing banks more context to approve, rather than defaulting to a decline

Don’t Forget the Checkout Itself

Even a perfectly configured acquiring setup loses conversions if the checkout experience is clunky. A few practical priorities:

- Payment forms need to work flawlessly on mobile most transactions happen there now

- Local payment methods matter more than ever: PIX in Brazil, iDEAL in the Netherlands, Alipay in China

- Checkout under ten seconds is the baseline expectation in 2026 anything slower bleeds abandonment

Fraud, Fees, and the Compliance Side of Things

Risk management and cost control aren’t the most exciting parts of payment strategy. But ignoring them is expensive.

Fraud Tools Have Moved On Has Your Setup?

Static fraud rules that flag transactions based on fixed thresholds are increasingly easy for bad actors to work around. Machine learning-based detection adjusts continuously, catching patterns that rule-based systems miss.

3D Secure 2.0 is now a compliance requirement across much of Europe under Strong Customer Authentication rules, and its reach is growing. When calibrated correctly, it shifts fraud liability away from the merchant while adding minimal friction for genuine customers. The balance matters too aggressive and real customers get blocked unnecessarily.

Chargebacks are their own problem. Monitoring thresholds have tightened, and exceeding them can trigger processing restrictions. Prevention is consistently cheaper than dispute resolution.

What Processing Actually Costs

The headline rate is rarely the full story. The real cost of acquiring card payments typically includes:

- Interchange fees: Set by card networks, usually the largest component

- Service charges: Monthly fees, per-transaction costs, and extras from the acquirer

- Chargeback and compliance fees: These add up faster than most merchants expect

- FX markups: Many processors apply opaque markups on cross-border payments; platforms offering transparent interbank rates can save meaningful money at volume

High-volume merchants generally those processing over $100,000 per month are usually in a position to negotiate directly with their acquiring bank. Lower chargeback ratios strengthen that negotiating position considerably.

Picking the Right Card Payments Acquirer for Where You’re Headed

The best acquirer isn’t the one with the lowest advertised rate. It’s the one whose strengths match the merchant’s transaction mix, customer geographies, and risk profile.

Larger merchants often benefit from direct acquiring bank relationships more flexibility on fees, better settlement speed options. Smaller businesses usually find payment service providers more practical, since they bundle acquiring, gateway, and risk management into one contract.

Either way, the arrangement needs regular review. Authorization rates shift. Fee structures change. A provider that was the right fit two years ago may not be anymore. Checking in every six months looking at approval rates, decline reasons, chargeback ratios, and total cost keeps the strategy grounded in current reality rather than outdated assumptions.

Wrapping Up

Getting acquiring card payments right in 2026 comes down to one shift in mindset: stop treating it as infrastructure and start treating it as strategy. Multi-acquirer setups, smarter routing, honest cost tracking, and fraud tools that actually keep pace with threats these aren’t optional upgrades for global merchants. They’re the baseline. The businesses that review, adjust, and optimize their payment stack regularly are the ones that convert more, lose less, and scale cleaner.

Conclusion

Acquiring card payments in 2026 is no longer something merchants can afford to ignore or “set and forget.” It sits directly at the intersection of revenue, risk, and customer experience. The difference between a high-performing payment stack and an average one often comes down to small but compounding factors better routing, higher authorization rates, lower fraud exposure, and faster checkout experiences.

Merchants that rely on a single acquirer or outdated setup are quietly losing conversions and margin. In contrast, businesses adopting multi-acquirer strategies and payment orchestration are gaining flexibility, improving approvals, and reducing dependency on any single provider. The shift is clear: payments are no longer just infrastructure they are a competitive advantage.

Regular optimization is what separates scalable systems from stagnant ones. Monitoring approval rates, reviewing fee structures, and adapting to regional payment preferences ensures that your setup evolves alongside your growth. In a global, fast-moving commerce environment, the merchants who treat acquiring as an ongoing strategy will consistently outperform those who don’t.

Frequently Asked Questions

What are acquiring card payments?

Acquiring card payments refer to the process where a merchant accepts card payments through an acquiring bank or payment provider. The acquirer processes transactions, communicates with card networks and issuing banks, and ensures funds are settled into the merchant’s account.

Why is having multiple acquirers important?

Using multiple acquirers reduces risk and improves performance. It allows merchants to route transactions based on geography, card type, and real-time success rates, leading to higher approval rates and less downtime impact.

What is payment orchestration?

Payment orchestration is a system that connects multiple payment providers and acquirers into one platform. It intelligently routes transactions to the best-performing provider, improving authorization rates and reducing costs.

How can I improve my card approval rates?

Approval rates can be improved by using local acquiring, enabling network tokenization, and sending enriched transaction data such as customer details and device information. These help issuing banks better assess and approve transactions.

VISIT MORE: APEX MAGAZINE